- Start Date

- Duration

- Format

- Language

- 20 Oct 2025

- 3 days

- Class

- Italian

L’utilizzo di piattaforme digitali di ultima generazione per la gestione dei servizi finanziari e assicurativi.

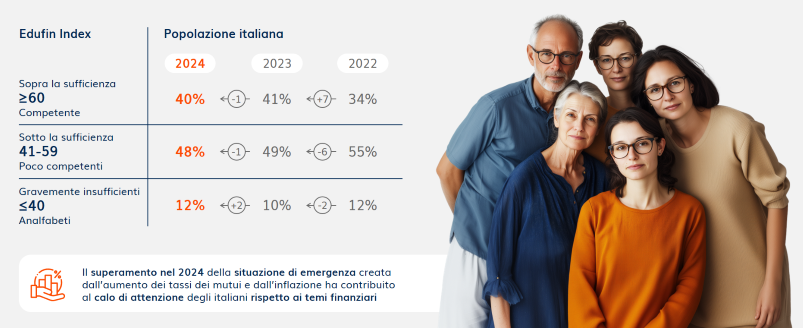

The average level of financial and insurance literacy among Italians is still too low to enable them to face an unstable and complex economic environment. With an average score of 55.6 out of 100, below the passing threshold of 60, the Edufin Index 2024, developed by SDA Bocconi in collaboration with Alleanza Assicurazioni and Fondazione Gasbarri, shows a slight dip compared to the previous year.

Some of the reasons for this unsatisfactory result are the lack of structured financial education in the school system, an unfavorable economic and geopolitical context, and limited trust in financial institutions. Added to all this is the absence of coherent strategies to effectively engage all population segments, making an already suboptimal situation even worse.

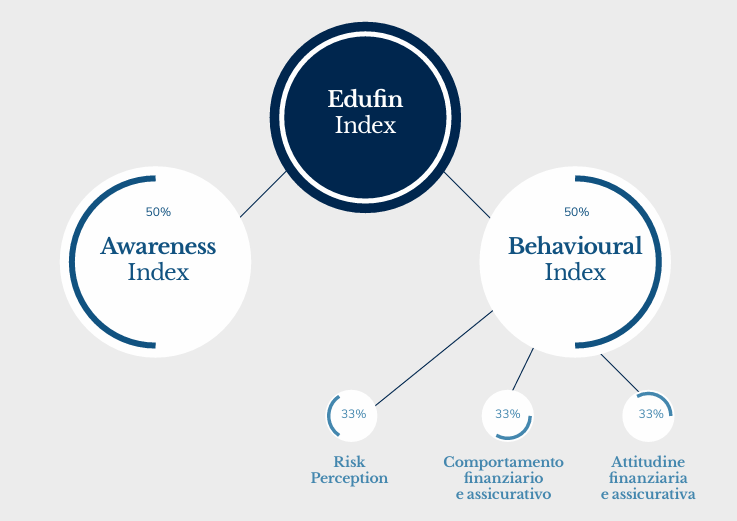

The study provides insights into the level of financial literacy among Italians. While the Edufin Index ties into institutional surveys conducted by CONSOB and the Bank of Italy, it stands out by extending its scope beyond the financial sector to include the insurance sector. What’s more, our index delves more deeply into measuring behavioral aspects.

In fact, the Edufin Index is based on two pillars, each contributing equally to the final score: an Awareness Index, which measures knowledge, and a Behavioral Index, which measures what we call behavioral composure—Italians' ability to make informed and responsible financial decisions.

Both components showed slight declines compared to the previous year. The Awareness Index scored 53.6, revealing insufficient knowledge of basic financial and insurance concepts among much of the population. This reflects not only an educational deficit but also Italians’ difficulty in recognizing and adequately assessing their financial skills.

The Behavioral Index, which measures the actual ability to act consciously in the financial field, dropped to 57.5. Specifically, Italians’ financial choices are influenced by an uncertain macroeconomic context and often incorrect risk perception, as evidenced by low scores in the “risk perception” sub-indicator. This aspect is crucial because poor risk perception can lead to unsound decisions with negative consequences, both in personal and economic terms.

The survey was conducted through a questionnaire designed by SDA Bocconi and administered by DOXA to about 3,500 individuals. To ensure more reliable comparisons, about half of the sample overlapped with the previous year’s sample.

The gap between northern and southern Italy is also evident in financial literacy. Residents of the Northeast achieved the highest scores, averaging 57.6, while people living in the South and on the islands lagged behind at 53, a difference of over four points. This reflects not only economic disparities but also unequal access to educational opportunities and financial advice.

Income also plays a decisive role. Higher earners (€80,000+ per year) averaged 64.8 on the index, well above the threshold, while respondents with incomes below €20,000 scored 50.3, signaling a high risk of financial exclusion.

Particularly concerning is the fact that 12% of the population averaged less than 40. This group includes socially vulnerable individuals who have no access to financial services. Among them, young people and women are overrepresented—two categories with specific challenges that deserve further analysis in the coming weeks.

The report divides the population into five distinct clusters based on financial literacy levels and associated behaviors:

The general results suggest that Italians’ low financial literacy can be explained by a combination of factors:

The SDA Bocconi faculty members involved in the creation of the EDUFIN INDEX 3° EDIZIONE Consapevolezza e comportamenti finanziari e assicurativi degli italiani (EDUFIN INDEX 3rd EDITION Financial and Insurance Literacy of Italians: Awareness and Behavior) report include Barbara Alemanni, Paola Castelli, Umberto Filotto, Gennaro De Novellis and Alessandro Recla.

L’utilizzo di piattaforme digitali di ultima generazione per la gestione dei servizi finanziari e assicurativi.

Conoscere logiche e strumenti dei processi di pianificazione finanziaria e dell'elaborazione, redazione e implementazione di un Piano Finanziario.

Per fornire logiche e principi per definire il modello di controllo aziendale e strumenti di analisi statistica a supporto delle previsioni e dei processi decisionali